Fed Cuts Rates, Will Mortgage Rates Follow in 2025?

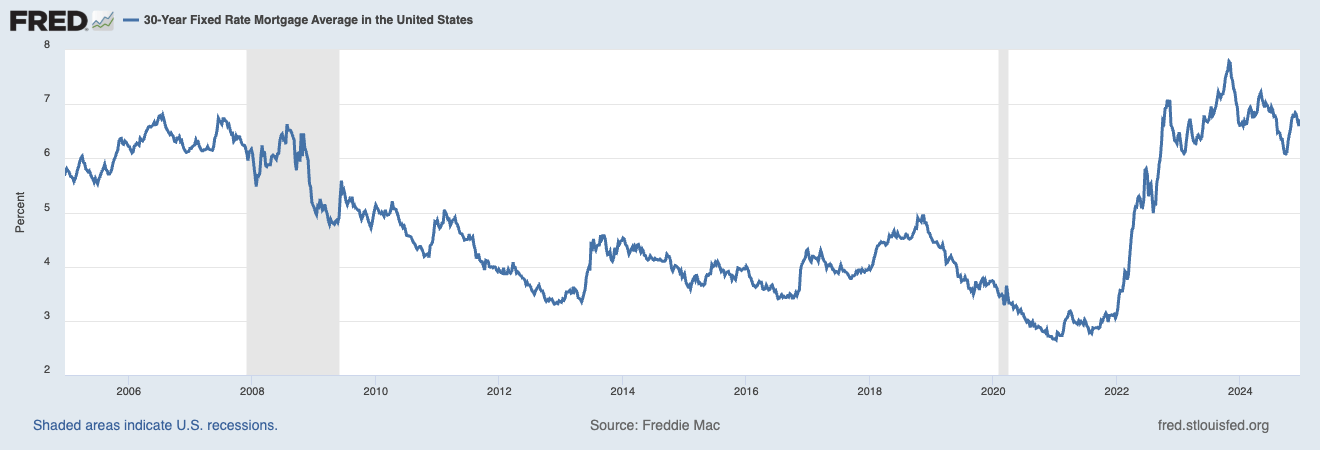

The Federal Reserve Cut the short term federal funds rate by 0.25% to a range of 4.25%-4.50%. Yet mortgage rates actually increased after the Federal Reserve cut short term interest rates.

Have you ever wondered why mortgage rates, which are the interest you pay on home loans, aren’t getting lower like they used to in the past? Let's break it down in simple terms.

In a Nutshell

Mortgage rates probably won’t drop back to the 3-4% range anytime soon because:

-

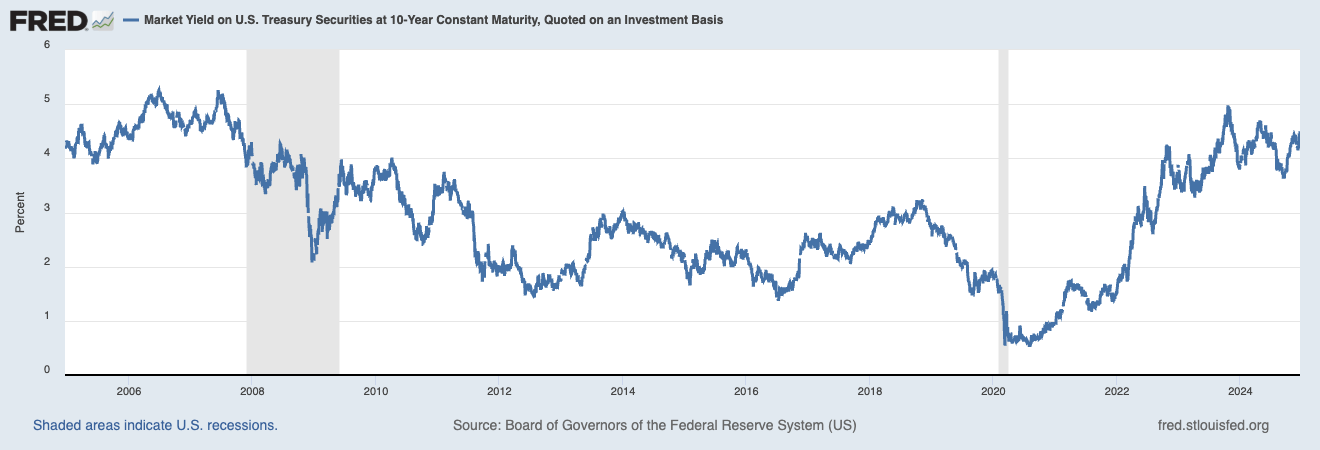

Mortgage rates follow the 10-Year Treasury yield, not the Fed’s short-term rate

-

Inflation is still a problem, so investors are moving away from bonds.

-

Bond prices and yields move in opposite directions. When prices fall, yields go up, which pushes mortgage rates higher.

-

The Fed’s pandemic bond-buying spree is over, and now they’re selling bonds instead.

-

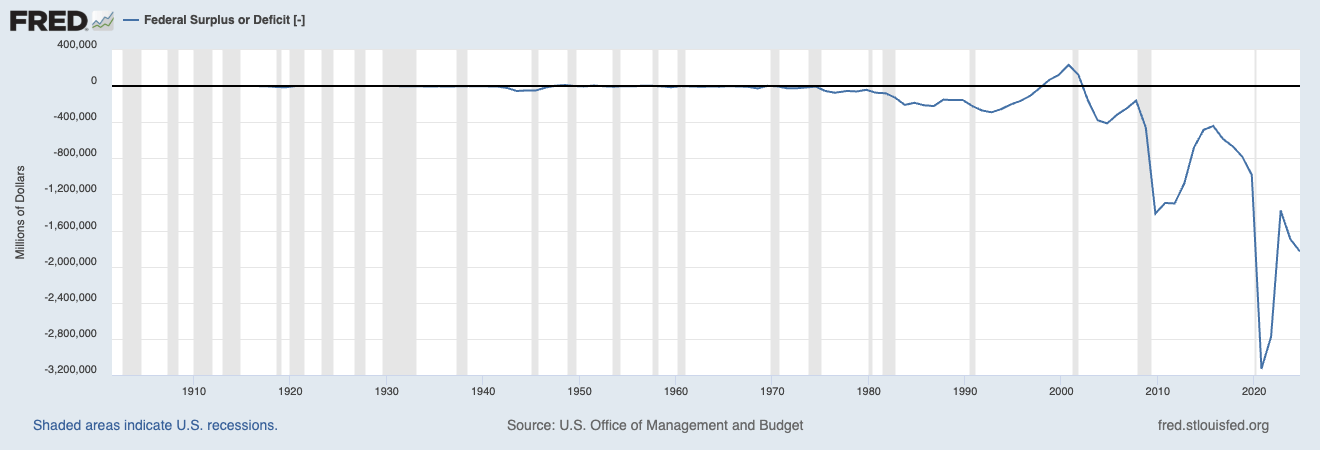

The government is running a deficit, so it has to sell more bonds, which keeps yields high.

Read on for the full break down

Mortgage rates are a bit like a see-saw. They go up and down based on different factors

The main factor that moves mortgage rates up and down is whats called the ten year treasury yield.

This is derived by an investment instrument called the U.S. Treasury Bond. A bond is a loan (or IOU) from the U.S. Government to investors.

For example, if you wanted to earn a profit on cash you have available, but don't want to invest into riskier assets like stock or crypto, you could buy a 10 Year Treasury Bond from the U.S. Government.

In exchange for letting the government borrow your cash, the government will pay you say, 4.5% annual interest on your money every 6 months. At the end of 10 years you get your entire initial investment back.

This 4% interest rate that the U.S. Government is offering in exchange for loaning them that money, is what's called the yield.

Why Investors Buy U.S. Treasuries

The risk of losing your investment is much lower, than investing in say an individual business through stock.

U.S. treasuries are considered the safest investment an investor can make since the U.S. government has never defaulted on its debt obligations (on top of being the most wealthy country in the world).

Why Does the U.S. Government Sell U.S. Treasuries?

The U.S. government issues treasury bonds to finance government spending whenever the federal budget is in a deficit.

The U.S. Federal Government is in a deficit when the government brings in less tax revenue from tax payers like workers and businesses, than it spends on government services like healthcare, social security payments, & building/repairing public owned buildings and facilities like roads, bridges and parks.

When the government is in a surplus, it means there is more tax funds coming into the government than it is spending.

Why Mortgage Rates will not drop into the 3-4% range we experienced during the COVID Pandemic in 2025 or even 2026.

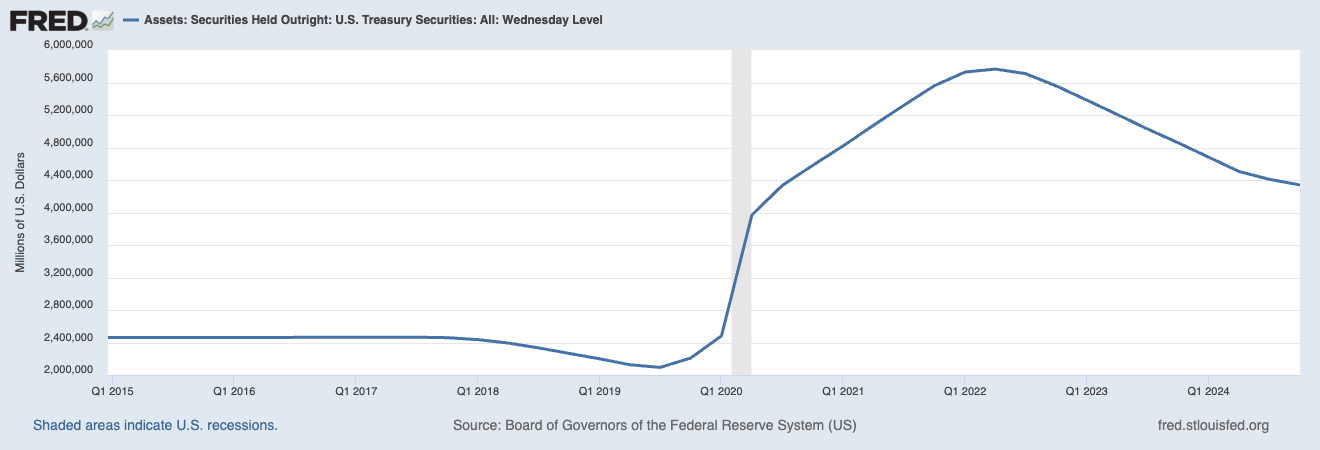

To understand why rates aren’t dropping, we need to think about what happened during COVID-19. Back then, the Federal Reserve bought a lot of these bonds to pump money into the economy to help keep it running. Think PPP loans, think stimulus checks, supplementary unempoyment insurance, etc.

Let's take a look at the huge amount of bonds the Federal Reserve was buying during the Pandemic:

When Large Amounts of Bonds are Purchased, Bond Yields Fall

That's because the bond market is driven the same as any other market based asset: supply and demand. When more investors are buying bonds than are being sold, it causes the price of these bonds to go up.

When the price of bonds go up, the government doesn't need to offer higher interest rates (yield) to entice investors to buy the bonds to finance government debt. There are plenty of buyers, which allows the government to offer lower yields.

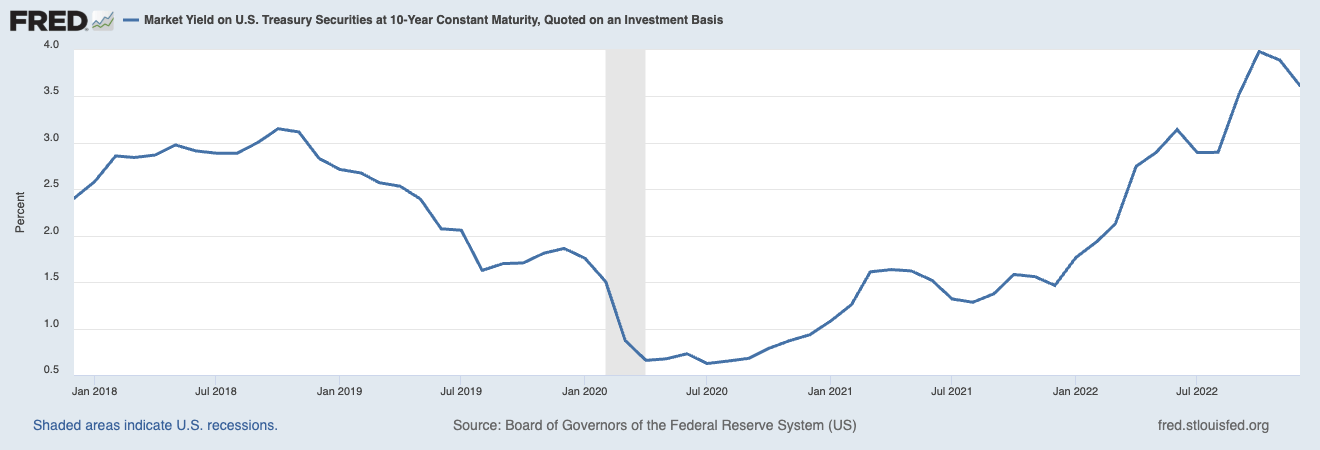

Check out the yield below of the 10 year treasury when the Federal Reserve was purchasing bonds during the pandemic:

Mortgage Rates & Home Affordability Take a Hit as the Fed Continues it's Fight Against Inflation

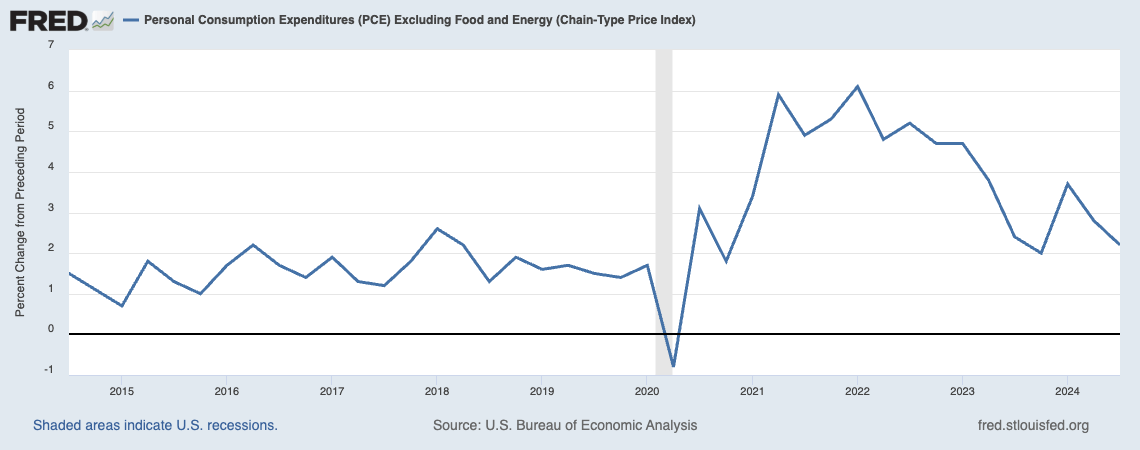

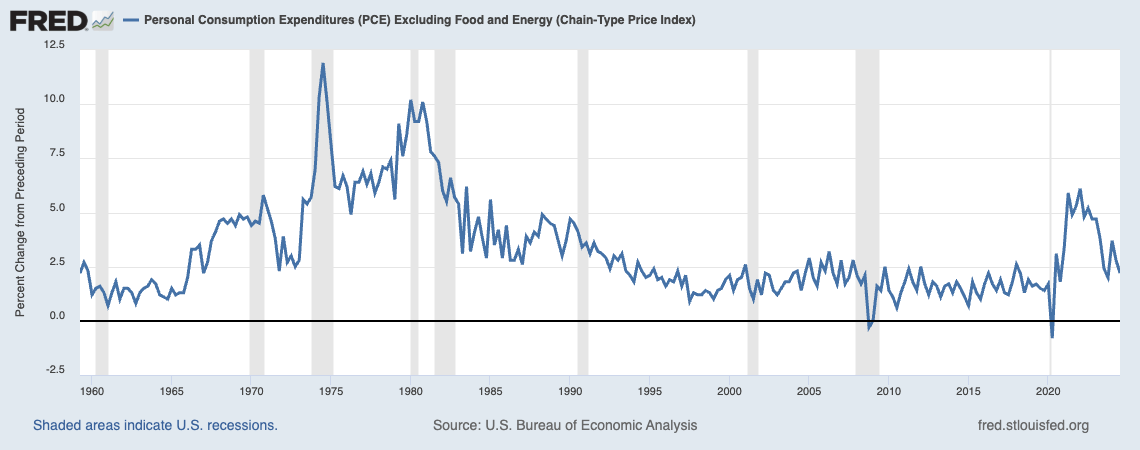

But now, because prices on everything went up (a.k.a. inflation) after the pandemic, the government has been selling treasuries to help remove money out of the economy to bring down inflation

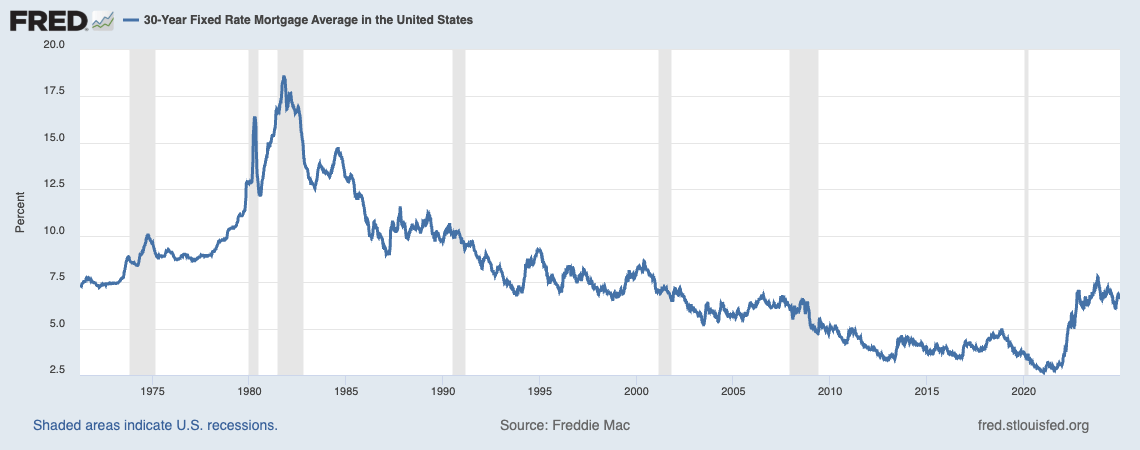

This is an attempt to avoid inflation spiking to catastrophic levels seen in the 70's & 80's's when the U.S. experienced life sucking inflation. This is also the period when mortgage rates hit their all time highs into the 18%s.

This move to fight inflation, has caused mortgage rates to increase as the Fed allows bonds to roll off it's balance sheet.

Summary

Mortgage rates are not likely to fall to the 3-4% range seen during the COVID pandemic due to a variety of factors:

- Mortgage rates follow the yield of the 10 Year U.S. Treasury, not the short term Federal Funds Rate that the Federal Reserve controls

- Inflation concerns are not yet fully controlled in the economy, as a result investors are selling bonds to move into riskier assets such as stock, real estate and crypto in attempt to outpace inflation

- Bond prices & yields have an inverse relationship; when more investors sell bonds than buy, it causes the price of those bonds to go down, and the yield to go up. This causes mortgage rates to go up

- The historically low mortgage rates seen during the COVID pandemic were in large part, a result of the Federal Reserve buying astronomical amounts of U.S. Treasuries to fund stimulus & mortgage bonds, pushing the price of the bonds up and lowering the yields to historic lows

- The Fed now has to reverse the enormous amount of financial stimulus provided during the pandemic by selling off or letting their bond holdings roll off their balance sheet without reinvestment.

- The U.S. Government is still spending more in government services than it brings in in tax revenue. The government will need to create more Treasuries to sell off and finance this debt. This increase in supply is likely to cause bond prices to drop and yields to rise (or not drop as much), resulting in an increase in mortgage rates

So, for now, mortgage rates are staying high because of these big money moves and choices. If we want to see them go down, some big changes would have to happen in how the government handles its money and bonds.

Hope this helps! If you found value in this post, drop your email below to stay in the loop on all things Real Estate, Mortgages & Finance!

Categories

Recent Posts